So after 250 posts, almost 4 years and dozens of page views I'm calling it quits. Our family is about to double in size (twins!) and unpaid market analysis is on the bottom rung of priorities.

Some final thoughts:

While I think some of the bear blogs are overstating the downside risk to the market from factors such as demographics and CMHC underwriting I do believe that growth in mortgage credit and prices will require some level of nominal price declines. This will take time.

Right now the Alberta real estate market is in a sort of limbo. The hangover from the rapid increase in price still lingers with elevated levels of foreclosures and high debt levels. In migration and employment growth are currently positive which are offsetting this right now but global economic risks add uncertainty.

My advice would be wary of advertisers selling mortgage that are engineeringed to look cheaper than rent but aren't. Or hucksters using poor reasoning to pump a boom that isn't happening. On the other hand it is important not mindlessly cheer on those who say the job recovery is fake or that economic armagedon is around the corner. Perhaps this appeal to balance is a little condescending and I should give more credit to the majority of people who are capable of thinking critically (I am an optimist). I wish I could offer a more definitive closing but that just isn't my style.

Thanks to all who stopped by over the years and contributed to the discussion. Best of luck to all.

Friday, July 8, 2011

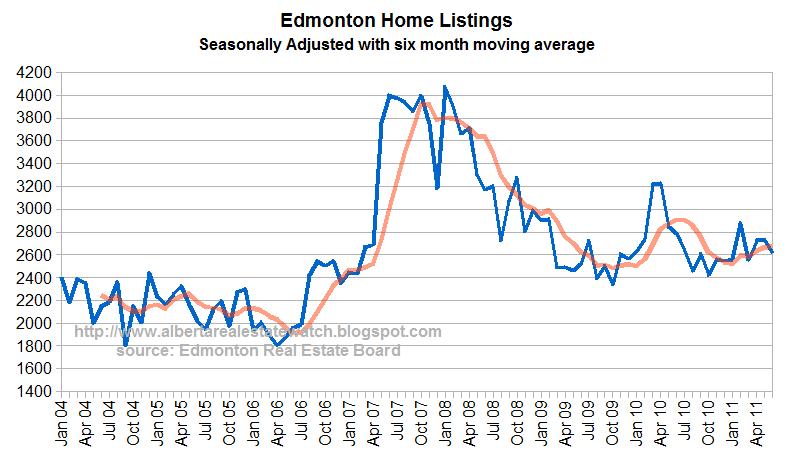

Edmonton Stats June 2011

Sales have dropped somewhat which could be expected for this time of year. Even with this drop the rate has maintained some gains from the dismal levels seen this time last year.

Listings dropped as expected in June.

Seasonally adjusted sales are low historically but they have been worse. This is a range similar to before the boom but above crisis levels.

The relatively low level of listings is having a stabilizing effect on the market.

The sales to new listing ration is slightly above 50%. A rate of 50% indicates a market with stable prices.

Listings dropped as expected in June.

Seasonally adjusted sales are low historically but they have been worse. This is a range similar to before the boom but above crisis levels.

The relatively low level of listings is having a stabilizing effect on the market.

The sales to new listing ration is slightly above 50%. A rate of 50% indicates a market with stable prices.

Saturday, June 18, 2011

Blast from the Past

- At the end of 2009 I had this exchange with Garth where he discussed how the Bank of Canada hiking rates would impact mortgage payments. He thought a 5-year fixed rate would be close to 7% as they move lockstep with the BoC. He had also argued there would be no more discounts available for some reason.

and that by this time a year from now BoC rate will be sitting at almost 1.6%, higher than today by 1.3%. That doesn't sound like a lot, but it puts the lowest VRM at 3.55% – which increases the monthly on a $400,000 loan by $300. A five-year mortgage would like go for close to 7%. Barn door. Horse.

#5 BearClaw on 12.16.09 at 9:47 pm

Garth,

I don’t think 5 year mortgages will be close to 7% with only a 1.3% increase in rates. 5 year mortgages are about 4% right now. An increase of 1.3% will put them at 5.3%.

There is a large spread between variable and fixed because there is some anticipation of rate increases priced in. So fixed rates may be less than 5.3% in this scenario.

Posted rate is 5.49% now at all majors. We are on the way back to 8% money in a few years. Get used to it now. — Garth

- #7 BearClaw on 12.16.09 at 9:54 pm

“The first hike will be at least a half, and probably a full load. That could raise VRMs overnight by 1% “or a little more than 44%. Ouch.”

Garth,

For a 25 year amortization it would raise the *total* payment by 12%. The interest portion would increase by 44%.

A 1% increase on a 2.25% rate is 44%. I did not mention payments. — Garth

- #10 BearClaw on 12.16.09 at 10:03 pm

"Posted rate is 5.49% now at all majors. We are on the way back to 8% money in a few years. Get used to it now.” -Garth

I think you know the difference between discounted and posted rates. But who cares? That’s not entertaining.

Kiss discounts goodbye as the BoC moves. That’s not entertaining either. — Garth

- #11 Siberta on 12.16.09 at 10:16 pm

You ain’t going to win on this site BearClaw, get used to it. You recently purchased to, if I remember correctly.

- #12 lgre on 12.16.09 at 10:21 pm

Bearclaw is learning that GT has every angle covered, dont bother trying to come from the back.

The ‘we are different’ theory is getting boring, nothing is different but everything is and will be the same…just wait for it.

Thursday, June 9, 2011

Canadian Recession and Recovery

From Stephen Gordon at Worthwhile Canadian Initiative:

The investment recovery was in two stages. In late 2009 and early 2010, expenditures were concentrated in the residential construction sector, but housing has played almost no role in the last four quarters. Happily, fixed business investment - and especially expenditures on machinery and equipment - started picking up just as the housing sector stopped contributing to growth.

See previous posts: here, here and here

Monday, June 6, 2011

Edmonton New Construction Stats May 2011

There were 2,974 single family homes under construction in Edmonton during April. This is less than half of the amount of construction during the peak (6,528) but up from the low reached during the recession (1,764).

There were 2,974 single family homes under construction in Edmonton during April. This is less than half of the amount of construction during the peak (6,528) but up from the low reached during the recession (1,764). Looking at all types of dwelling under construction shows less of a rebound because the condo glut took longer to work off and new starts having been slower to recover. In fact there remains a surplus of completed and not absorbed units when considering all types of construction other than single family (shown in dark gray).

Looking at all types of dwelling under construction shows less of a rebound because the condo glut took longer to work off and new starts having been slower to recover. In fact there remains a surplus of completed and not absorbed units when considering all types of construction other than single family (shown in dark gray). link

Saturday, June 4, 2011

Edmonton Sales

The story: Sales increased from crisis levels but are still low historically. New listings have been relatively tame and inventory is down year over year.

Tuesday, May 31, 2011

Population Aging and Housing Demand

Recently the Stephen Gordon wrote about how immigration cannot fix the aging problem on the Worthwhile Canadian Initiative Blog. The main point was the number of immigrants required is too overwhelming to overcome the enormous gap as shown in the chart below.

Ben at Financial Insights also commented on this analysis as it related to housing:

In this projection the pyramid is skewed up, as the baby boomers age, but also increases for the younger age groups, albeit to a lesser degree. The future will certainly have more seniors but the decline in housing demand is fully offset under moderate immigration, fertility and life expectancy assumptions.

See previous post here.

Ben at Financial Insights also commented on this analysis as it related to housing:

The current immigration rate is wholly inadequate in eliminating the coming demographic imbalance. While it certainly helps, it will be insufficient in entirely eliminating the headwind on house prices set to be exerted by the aging population.The post at Worthwhile Canadian Initiative derived the amount of immigration required to avoid population aging. This is far more than the what would be required to maintain a constant level of housing demand. This is an important distinction and is best represented in the chart below from Statistics Canada population projections (Medium growth).

In this projection the pyramid is skewed up, as the baby boomers age, but also increases for the younger age groups, albeit to a lesser degree. The future will certainly have more seniors but the decline in housing demand is fully offset under moderate immigration, fertility and life expectancy assumptions.

See previous post here.

Sunday, May 8, 2011

Business Credit Expanision and Economic Recovery in Canada

Since the recession ended the role of household credit in the recovery has been examined. One narrative that has formed is that this is largely artificial due to an unsustainable rate of household credit expansion.

However, not much attention has been given to role of business credit shown in the chart below.

Consider three different time periods in recent history.

(A) Pre-recession household and business credit were expanding at a rate of 11.8% and 8.6% respectively.

(B) In the aftermath of the financial crisis household credit growth slowed to a rate of 7.4% while business credit expansions stopped entirely with an yearly growth rate of -0.1%.

(C) Recently, household credit growth has eased to 6.5% while business credit recovered to 4.8%.

The financial crisis had a bigger impact on business credit than household credit and since then the gap between the two has narrowed considerably. This could explain some of the continued strength of the Canadian economy after two years of recovery.

Source: Bank of Canada

household credit

business credit

However, not much attention has been given to role of business credit shown in the chart below.

Consider three different time periods in recent history.

(A) Pre-recession household and business credit were expanding at a rate of 11.8% and 8.6% respectively.

(B) In the aftermath of the financial crisis household credit growth slowed to a rate of 7.4% while business credit expansions stopped entirely with an yearly growth rate of -0.1%.

(C) Recently, household credit growth has eased to 6.5% while business credit recovered to 4.8%.

The financial crisis had a bigger impact on business credit than household credit and since then the gap between the two has narrowed considerably. This could explain some of the continued strength of the Canadian economy after two years of recovery.

Source: Bank of Canada

household credit

business credit

Saturday, May 7, 2011

Edmonton Stats April 2011

The REALTORS Association of Edmonton released their monthly stats here and overall they show weak sales and normal level of new listings.

The preliminary number for sales held steady with 1487 in April compared to an initial report of 1503 in March. Normally, sales are expected to increase this time of year. Preliminary sales are at scorched earth level, which is equivalent to the worst six months of the financial crisis.

The preliminary number for sales held steady with 1487 in April compared to an initial report of 1503 in March. Normally, sales are expected to increase this time of year. Preliminary sales are at scorched earth level, which is equivalent to the worst six months of the financial crisis.

Listings are rising at a normal pace for spring.

Listings are rising at a normal pace for spring.

Seasonally adjusted rate of sales have been low for a year following a bounce after the financial crisis. I assumed the final number for sales will come in about 7% higher than the preliminary figure.

Seasonally adjusted rate of sales have been low for a year following a bounce after the financial crisis. I assumed the final number for sales will come in about 7% higher than the preliminary figure.

Seasonally adjusted listings have been stable since a spike last spring.

With lower sales and stable listings on a seasonally adjusted basis the sales to new listing ratio fell to 47%. A ratio lower than 50% indicates a market with downward price pressure.

Finally a historical chart of actual sales, listings and inventory.

The preliminary number for sales held steady with 1487 in April compared to an initial report of 1503 in March. Normally, sales are expected to increase this time of year. Preliminary sales are at scorched earth level, which is equivalent to the worst six months of the financial crisis.

The preliminary number for sales held steady with 1487 in April compared to an initial report of 1503 in March. Normally, sales are expected to increase this time of year. Preliminary sales are at scorched earth level, which is equivalent to the worst six months of the financial crisis. Listings are rising at a normal pace for spring.

Listings are rising at a normal pace for spring. Seasonally adjusted rate of sales have been low for a year following a bounce after the financial crisis. I assumed the final number for sales will come in about 7% higher than the preliminary figure.

Seasonally adjusted rate of sales have been low for a year following a bounce after the financial crisis. I assumed the final number for sales will come in about 7% higher than the preliminary figure.

Seasonally adjusted listings have been stable since a spike last spring.

With lower sales and stable listings on a seasonally adjusted basis the sales to new listing ratio fell to 47%. A ratio lower than 50% indicates a market with downward price pressure.

Finally a historical chart of actual sales, listings and inventory.

Monday, April 18, 2011

Alberta Population Report Q4 2010

The Alberta population report for the Q4 2010 was released last month here.

On a quarterly basis Alberta's population grew by 0.21% in Q4 2010.

7,249 natural growth (births - deaths)

2,510 net interprovincial migration

4,633 net international migration

-6,725 net non-permanent residents (!)

The exodus of non-permanent residents was offset by international and interprovincial immigration.

On a quarterly basis Alberta's population grew by 0.21% in Q4 2010.

7,249 natural growth (births - deaths)

2,510 net interprovincial migration

4,633 net international migration

-6,725 net non-permanent residents (!)

The exodus of non-permanent residents was offset by international and interprovincial immigration.

Sunday, April 17, 2011

Edmonton New Construction Update

The number of single family homes under construction in Edmonton has decreased from 4,116 in July to 3,212 in February. Starts have fallen over 50% YOY while completions increased by 60%.

The amount of units under construction or unabsorbed for all types of residential structures has decreased for 5 consecutive months.

The amount of units under construction or unabsorbed for all types of residential structures has decreased for 5 consecutive months.

Wednesday, April 13, 2011

The Canadian Job Recovery is Real

From Greater Fool

And From Financial Insights:

Real estate sales are down, mortgage rules tighter, gas is $1.40 a litre and the latest jobs numbers suck.more here

And From Financial Insights:

This has been a constant criticism of mine with regards to the ‘rebound’ in employment from the recession lows. It has overwhelmingly been driven by growth in construction jobs, public sector jobs, and part time jobs…..not overly impressive.The idea that the jobs recovery is somehow fake is something I have covered in previous posts (here and here ). While this recovery has had a disproportionate increase in construction, it has not made up anywhere near the majority of jobs. The other claim regarding public sector and part time jobs is false.

Monday, April 4, 2011

Calagry Stats for March 2011

Bob Truman updated the Old Criteria stats for March 2011. With this I have once again update the trends new listings and sales adding inventory and price charts as well this month. Seasonally adjusted sales and new listings as well as benchmarks are explained here.

Sales are down year over year but are still above the pace of the financial crisis (shown in red). There are two ways to interpret this YOY drop.

1) In terms of sales the market was doing reasonably well last March and it was only in June and July where they deteriorated. So if we maintain this same rate seasonally adjusted we can expect an increase in yearly sales shortly.

2) Now that there are fewer available buyers due to tighter mortgage rules the rate of sales should decrease faster than normal, resulting in continued year over year sales declines.

April will be a relatively slow month due to a sales vacuum formed by the recent mortgage rule changes. However I believe this will only have a short term impact and sales would then recover. My guess would be somewhere above last year's rate but below that of 2nd half of 2009, shown by the green line.

Listings are following closely the same rate as the 2nd half of 2009, shown in green. The low level of new listings is providing some support to the overall market which would be faring worse otherwise due to the low level of sales.

Inventory is about the same as this time last year, with only 0.6% fewer properties on the market. What is notable however is the difference in the rate of change between the first few months of this year compared to last.

Dec 2009: 5017

Mar 2010: 8524

% increase: 70%

Dec 2010: 6056

Mar 2011: 8477

% increase: 40%

Median prices are down 3.5% from last March.

Sales to new listing ratio is hovering around 50% from low sales and new listings.

Update: The Edmonton Journal ran an article on Don Campbell pumping another boom: “I’ve studied this for 19 years and I have not seen this strong of a perfect storm before.” See previous posts: part 1 and part 2.

Sales are down year over year but are still above the pace of the financial crisis (shown in red). There are two ways to interpret this YOY drop.

1) In terms of sales the market was doing reasonably well last March and it was only in June and July where they deteriorated. So if we maintain this same rate seasonally adjusted we can expect an increase in yearly sales shortly.

2) Now that there are fewer available buyers due to tighter mortgage rules the rate of sales should decrease faster than normal, resulting in continued year over year sales declines.

April will be a relatively slow month due to a sales vacuum formed by the recent mortgage rule changes. However I believe this will only have a short term impact and sales would then recover. My guess would be somewhere above last year's rate but below that of 2nd half of 2009, shown by the green line.

Listings are following closely the same rate as the 2nd half of 2009, shown in green. The low level of new listings is providing some support to the overall market which would be faring worse otherwise due to the low level of sales.

Inventory is about the same as this time last year, with only 0.6% fewer properties on the market. What is notable however is the difference in the rate of change between the first few months of this year compared to last.

Dec 2009: 5017

Mar 2010: 8524

% increase: 70%

Dec 2010: 6056

Mar 2011: 8477

% increase: 40%

Median prices are down 3.5% from last March.

Sales to new listing ratio is hovering around 50% from low sales and new listings.

Update: The Edmonton Journal ran an article on Don Campbell pumping another boom: “I’ve studied this for 19 years and I have not seen this strong of a perfect storm before.” See previous posts: part 1 and part 2.

Saturday, March 26, 2011

Don Campbell - Analyzing the sales pitch (II)

The last post covered the theme of Don Campbell's recent blog to sell seats at a weekend real estate course. He just had to inform Albertans of a pre-boom buying window before outsiders bought everything up first. The wording was selected carefully to only imply massive price appreciation while being open to interpretation to avoid future scrutiny. He reassured skeptics they could dramatically reduce risk by investing not speculating while still using upcoming price appreciation as a central incentive.

The argument for a return to higher prices was made with the 'Momentum Graph' shown below [emphasis mine].

exactly the amount of future price increases higher prices (edit). Note how it is referred to as a "formula" to give the false impression it is based on some serious scientific theory.

The Momentum Graph falsely claimed to show "exactly the progression of an economy and how it eventually impacts the Real Estate Market". I will provide some specific examples that contradicts this:

Radley showed that the 2006-2007 price appreciation went over and above any GDP growth here.

Ben at Financial Insights recently compiled a similar chart for the Canadian wide market.

The Edmonton Housing Bust Blog compared local condo prices to rents. In Don's momentum chart it shows that rent increases come first and then lead to higher prices. If this was applicable to the last boom this ratio should have fallen with higher rents initially then increase as prices caught up. Instead prices outpaced rents for the entire boom.

Now consider the Teranet Price Index at 3 points in time after the boom.

1) In mid-2007 there was positive GDP growth, a strong job market, population growth and rent increases. The 'Momentum Graph' would predict future price increases yet they were at their absolute peak.

2) In spring of 2009 GDP was lower after the oil bust and recession, combined with lower population growth and increasing Alberta unemployment. The 'Momentum Graph' doesn't go into reverse for obvious reasons, but if it did it sure wouldn't predict a bounce in prices.

3) In mid 2010 the Alberta economy and job growth have improved yet prices started trending down despite this.

Even if you accept some relation between GDP and house prices it is reckless not to mention that 2006-2007 was an anomaly. Don wants readers to make the connection with the GDP chart and another boom to pump his seminar, while being vague enough to provide future cover. Adding context is not helpful to his financial goals.

The argument for a return to higher prices was made with the 'Momentum Graph' shown below [emphasis mine].

Here's what you use to predict the real estate market future: The Momentum Graph, which shows exactly the progression of an economy and how it eventually impacts the Real Estate Market.This chart was constructed to be used conveniently with the GDP data from royal bank presented later. Putting the two together the reader can predict

The Economic Formula to Predict The Future

In a nutshell this graph states the following:

GDP growth >> Job growth >> Population growth >> Increased rental demand (12 months later) >> Increased rents >> Property purchase demand (18 months later) >> and eventually leads to property price increases.

The Momentum Graph falsely claimed to show "exactly the progression of an economy and how it eventually impacts the Real Estate Market". I will provide some specific examples that contradicts this:

Radley showed that the 2006-2007 price appreciation went over and above any GDP growth here.

Ben at Financial Insights recently compiled a similar chart for the Canadian wide market.

The Edmonton Housing Bust Blog compared local condo prices to rents. In Don's momentum chart it shows that rent increases come first and then lead to higher prices. If this was applicable to the last boom this ratio should have fallen with higher rents initially then increase as prices caught up. Instead prices outpaced rents for the entire boom.

Now consider the Teranet Price Index at 3 points in time after the boom.

1) In mid-2007 there was positive GDP growth, a strong job market, population growth and rent increases. The 'Momentum Graph' would predict future price increases yet they were at their absolute peak.

2) In spring of 2009 GDP was lower after the oil bust and recession, combined with lower population growth and increasing Alberta unemployment. The 'Momentum Graph' doesn't go into reverse for obvious reasons, but if it did it sure wouldn't predict a bounce in prices.

3) In mid 2010 the Alberta economy and job growth have improved yet prices started trending down despite this.

Even if you accept some relation between GDP and house prices it is reckless not to mention that 2006-2007 was an anomaly. Don wants readers to make the connection with the GDP chart and another boom to pump his seminar, while being vague enough to provide future cover. Adding context is not helpful to his financial goals.

Subscribe to:

Comments (Atom)